STOCK Act filing delay is the gap between when a member of Congress (or a covered spouse or dependent account) executes a reportable trade and when the public can read it. That gap is legal by design—not a data bug—and it is the single biggest reason congressional trade trackers should never be treated like live market feeds.

This guide explains the 30/45-day Periodic Transaction Report (PTR) rule, the extra lag before portals publish filings, how to measure delay in your own notes, and what a late filing does not prove. It is educational context, not investment advice.

The STOCK Act rule in plain language

The STOCK Act amended the Ethics in Government Act to require Periodic Transaction Reports (PTRs) for securities transactions over $1,000 by covered officials and certain family accounts.

For House filers, the House Committee on Ethics instruction guide states that a PTR is due by the earlier of:

- 30 days from when the filer becomes aware of the transaction, or

- 45 days from the transaction date.

The Senate follows the same core timing framework for PTR-style transaction reporting under its ethics and disclosure rules. The Senate eFD search portal is where published Senate PTRs land after filing.

Important nuance from the House PTR due-date calculator guidance: if a member personally executes a trade, the 30-day awareness clock often starts at the transaction itself. If a spouse or dependent account trades without immediate notice, the filer may rely on the 45-day outer deadline—but ethics guidance still recommends regular account checks so trades are not discovered only at the deadline edge.

Three dates researchers confuse

| Date | What it means | Why it matters |

|---|---|---|

| Transaction date | When the trade occurred | Price action you care about usually happened here |

| Filed date | When the PTR was submitted to the Clerk (House) or Senate ethics system | Measures compliance with the 30/45-day rule |

| Public posting date | When the disclosure appears on House or Senate search | What trackers ingest—often days after filing |

A tracker alert timestamp is a fourth clock: when your software first indexed the row. Always log which date you are looking at.

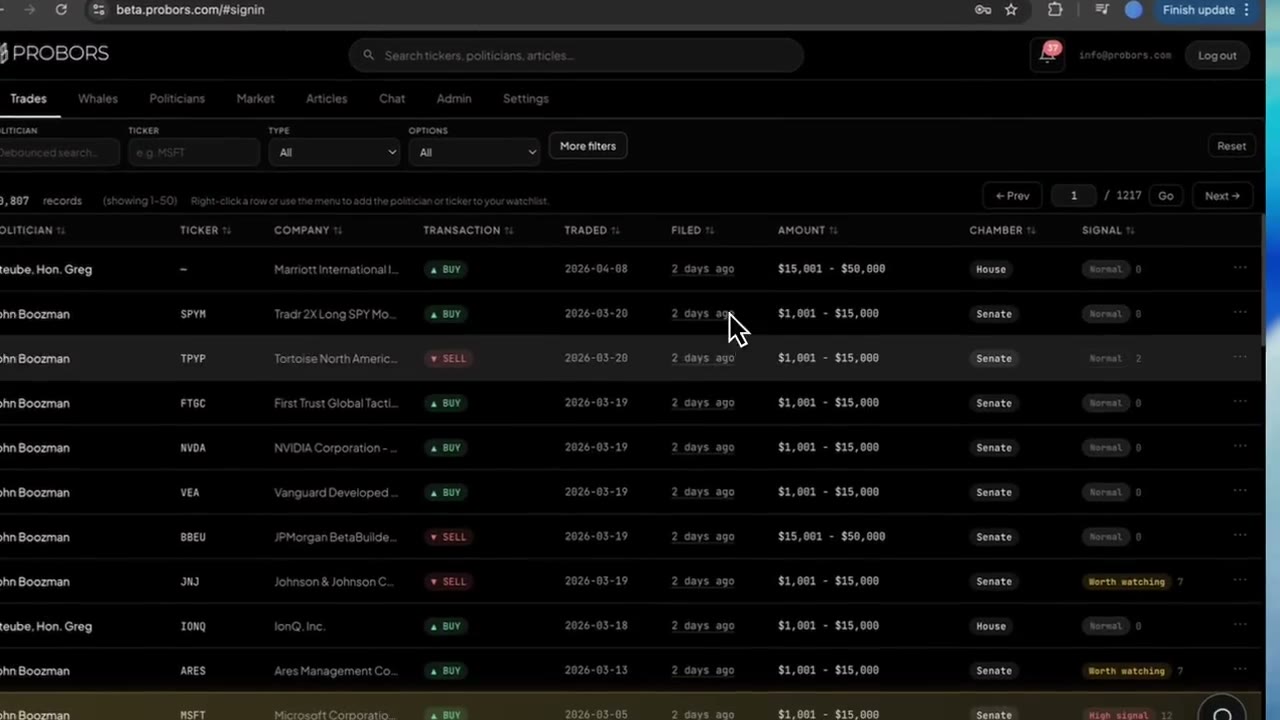

Real delay examples (ProBors production data, 2026-06-18 UTC)

Data pull: 2026-06-18T07:05:00+00:00

Source: Authenticated ProBors congressional disclosure snapshot

The table below uses verified rows from that pull. Delay = filed date minus transaction date.

| Politician | Ticker | Type | Transaction | Filed | Delay |

|---|---|---|---|---|---|

| Rep. Matthew Robert Van Epps | NVDA | Sale | 06/16/2026 | 06/17/2026 | 1 day |

| Rep. Matthew Robert Van Epps | MSFT | Sale | 06/16/2026 | 06/17/2026 | 1 day |

| Sen. John Boozman | MBB | — | 05/13/2026 | 06/16/2026 | 34 days |

| Sen. John Boozman | IEI | — | 05/13/2026 | 06/16/2026 | 34 days |

| Sen. John Fetterman | — | — | 05/06/2026 | 06/12/2026 | 37 days |

| Rep. Sheri Biggs | — | — | 04/28/2026 | 06/08/2026 | 41 days |

Across the 200-row sample, delays clustered as follows: 17 filings within 1 day, 28 within a week, 131 between 8–30 days, and 24 between 31–45 days. None in this slice exceeded 45 days—consistent with the statutory outer bound, not proof that late filings never happen elsewhere.

Fast filings (like the Van Epps rows) show that “congress trade” headlines can appear almost next-day when a member files promptly. Longer filings (30–41 days) are still timely under the STOCK Act even though the market moved weeks earlier.

Why delay exists (and why it is not going away soon)

Congressional disclosure was built for ethics transparency and conflict-of-interest monitoring, not for sub-second copy trading. The STOCK Act improved on annual-only reporting, but it deliberately kept a multi-week window.

Practical reasons delays persist:

- Broker notification lag — A member may not receive confirm notices the same day a spouse's account trades.

- Batch filing habits — Some offices file multiple PTR lines in one submission after month-end review.

- Portal processing — Even a same-day filing must be parsed, posted, and ingested by trackers.

- Range-based amounts — PTRs report dollar brackets, not share counts, which slows manual review before filing.

Reform bills occasionally propose shorter windows (for example 10-day ideas). Until law changes, researchers should model 30–45 days as the normal band.

How to measure filing delay in your workflow

- Record transaction date and filed date on every row you save.

- Compute delay days = filed − transaction.

- Note whether the trade was still inside the 45-day PTR deadline.

- Compare price change from transaction date to your alert date, not just filing date.

- Flag rows where delay exceeds ~30 days for extra skepticism—even if legal, edge has usually decayed.

On ProBors, trade detail and signal context surfaces filing delay so you can sort and filter without rebuilding the math in a spreadsheet. Signal scores treat long delays as lower urgency—see the trade signal scores guide.

Filing delay vs market “edge”

A 34-day delay does not automatically mean:

- The politician traded on material nonpublic information

- The filing was intentionally timed to hide activity

- You can still front-run the move when the alert fires

It does mean:

- Public market participants had weeks without this specific disclosure

- Any short-term price move tied to the transaction date is historical by the time you read the PTR

- Your research question should shift from “What happened yesterday?” to “Does this fit a pattern worth studying?”

What this data does NOT prove

The examples and buckets above are descriptive statistics from one production snapshot. They do not prove:

- That every member files within 45 days (enforcement and amendments happen; check the source PDF)

- That prompt filers are “better” traders or worse ones

- That delay length predicts forward returns

- That ProBors or any tracker captured the row at public posting time—ingestion adds its own minutes or hours

Always open the original House disclosure or Senate eFD record before treating a row as authoritative.

House vs Senate posting mechanics (short version)

| Chamber | Primary public search | PTR timing rule (summary) |

|---|---|---|

| House | disclosures-clerk.house.gov | Earlier of 30 days aware / 45 days from trade |

| Senate | efdsearch.senate.gov | Same core STOCK Act PTR framework |

House guidance also notes that PTRs must be posted within 30 days of filing—so a trade filed on day 45 may not be web-visible until roughly day 75 in a worst-case chain. Real-world posting is usually faster, but the stacked deadlines matter when you model total public lag.

FAQ

Is a 40-day filing “late”?

Often it is still compliant with the 45-day statutory outer deadline. “Late” in headlines usually means late relative to the trade, not late relative to ethics rules.

Do spouses and dependents affect delay?

Yes. Ethics guidance explicitly contemplates that a member may learn about a spouse trade days or weeks later, which pushes filings toward the 45-day boundary even when the member is diligent.

How is this different from Form 4 insider timing?

Insider Form 4s have their own SEC deadlines (often two business days for many events). Comparing congress PTR delay to Form 4 speed is apples-to-oranges—see how to read politician trade disclosures for congress-specific fields.

Does ProBors show delay on every row?

Where source dates exist, ProBors computes and displays filing delay in trade context and uses it in signal scoring. Missing or amended filings should be verified at the source.

Track filing delay on every congress row

Search STOCK Act disclosures on ProBors, compare transaction and filed dates side by side, and filter by signal score before you read the PDF.

Get startedRelated reading

Sources & methodology

Last updated:

ProBors uses public disclosure records, SEC filings, House and Senate financial disclosure portals, market data, and in-product workflow checks. Articles are written as research education, not investment advice.