Introduction

If you bought stock right before market moving legislation, earnings surprises, or government contracts, there’s a good chance your broker would flag it. If you did it repeatedly, regulators might call. And if you made millions doing it, you could be investigated.

Unless you’re a member of Congress.

This article breaks down real trading behaviors by politicians that would almost certainly raise red flags for everyday investors, yet remain legal under current rules. We are not talking about conspiracy theories or rumors. These are disclosed trades, reported publicly, and often weeks late.

Understanding how this system works matters because it exposes a massive gap between what is allowed for lawmakers and what is tolerated for the public. And once you see the pattern, it becomes hard to ignore.

Key Findings Overview

Here’s what consistently shows up in congressional trading data:

-

Politicians buying stocks days or weeks before major policy announcements

-

Heavy use of options, which amplify gains and limit disclosure clarity

-

Trades clustered around defense, tech, energy, and healthcare

-

Disclosure delays of 30 to 45 days, sometimes longer

-

No requirement to prove trades were independent of legislative knowledge

None of this is illegal under current law. That’s the problem.

What Would Trigger an Investigation for You

Let’s start with what happens to a normal investor.

If a retail trader consistently:

-

Buys stocks shortly before price moving news

-

Focuses on sectors tied to upcoming government action

-

Uses leverage or options for outsized gains

-

Repeats this pattern over time

That activity can trigger:

-

Broker compliance reviews

-

SEC surveillance flags

-

Requests for trade rationale

-

Potential insider trading investigations

Even being right too often can be a problem if the timing looks suspicious.

Now compare that to Congress.

The Trades That Look “Too Perfect”

Many congressional trades share the same features regulators look for elsewhere.

Extremely Convenient Timing

Examples seen repeatedly in public disclosures include:

-

Buying defense contractors before military funding increases

-

Buying semiconductor stocks ahead of chip legislation

-

Buying energy stocks before policy shifts or supply shocks

In the private sector, proximity to decision making plus trading equals scrutiny. In Congress, it equals a disclosure form weeks later.

Heavy Options Usage

Options are popular among lawmakers for a reason:

-

They amplify gains

-

They limit downside risk

-

They often require less precise disclosure

Seeing repeated call option purchases before rallies is not normal behavior for long term investors. It is, however, very common in congressional filings.

Sector Specialization

Many lawmakers repeatedly trade the same industries they regulate or oversee:

-

Defense committee members trading defense stocks

-

Tech regulation participants trading big tech

-

Healthcare lawmakers trading pharma

In corporate governance, this would be a compliance nightmare. In Congress, it is routine.

Source: https://www.finra.org/media-center/finra-unscripted/insider-trading-detection-program-update

Why It’s Legal for Them

The key protection is not innocence. It’s structure.

The STOCK Act Has Major Loopholes

While the STOCK Act technically bans insider trading by members of Congress, it:

-

Does not define what counts as material non public information clearly

-

Allows delayed disclosures

-

Has weak enforcement mechanisms

-

Rarely results in penalties

In practice, proving intent is nearly impossible.

Knowledge Is “Public Facing”

Lawmakers argue that:

-

They don’t control final outcomes

-

Policy discussions are ongoing

-

Markets already price in expectations

That defense would not work for corporate insiders. But Congress is not treated the same way.

Why This Would Never Fly for Retail

Imagine this scenario for a normal trader:

You work in an industry adjacent to a major company. You hear early signals that something big is coming. You buy options. The stock jumps. You repeat this several times a year.

Even without direct proof, regulators would look closely.

Now imagine doing that while writing the rules that affect the company.

That is the difference.

Patterns That Keep Appearing

When you zoom out, clear trends emerge:

-

Consistent market outperformance by politicians

-

Better timing than most professional funds

-

Higher use of leverage than typical retail traders

-

No meaningful consequences for late disclosures

This isn’t about one trade or one person. It’s about a system that allows asymmetric freedom.

Why People Are Angry

Public frustration is not partisan. It’s structural.

People are upset because:

-

Lawmakers shape markets and trade them

-

Disclosures arrive after the opportunity is gone

-

Penalties for late reporting are trivial

-

Retail investors play by stricter rules

The market is supposed to be fair. This feels like the opposite.

What This Means for Investors

You can’t change the rules overnight. But you can be aware.

Key takeaways:

-

Politician trades are signals, not guarantees

-

Timing matters more than headlines

-

Disclosure delays reduce usefulness

-

Patterns matter more than single trades

Tracking this data in real time is the only way to even the odds.

Conclusion

If you made these trades, you would probably be investigated. If a hedge fund did it, journalists would ask questions. When politicians do it, it’s called disclosure.

That disconnect is why this topic keeps going viral. It sits at the intersection of money, power, and accountability.

Until the rules change, transparency is the only defense.

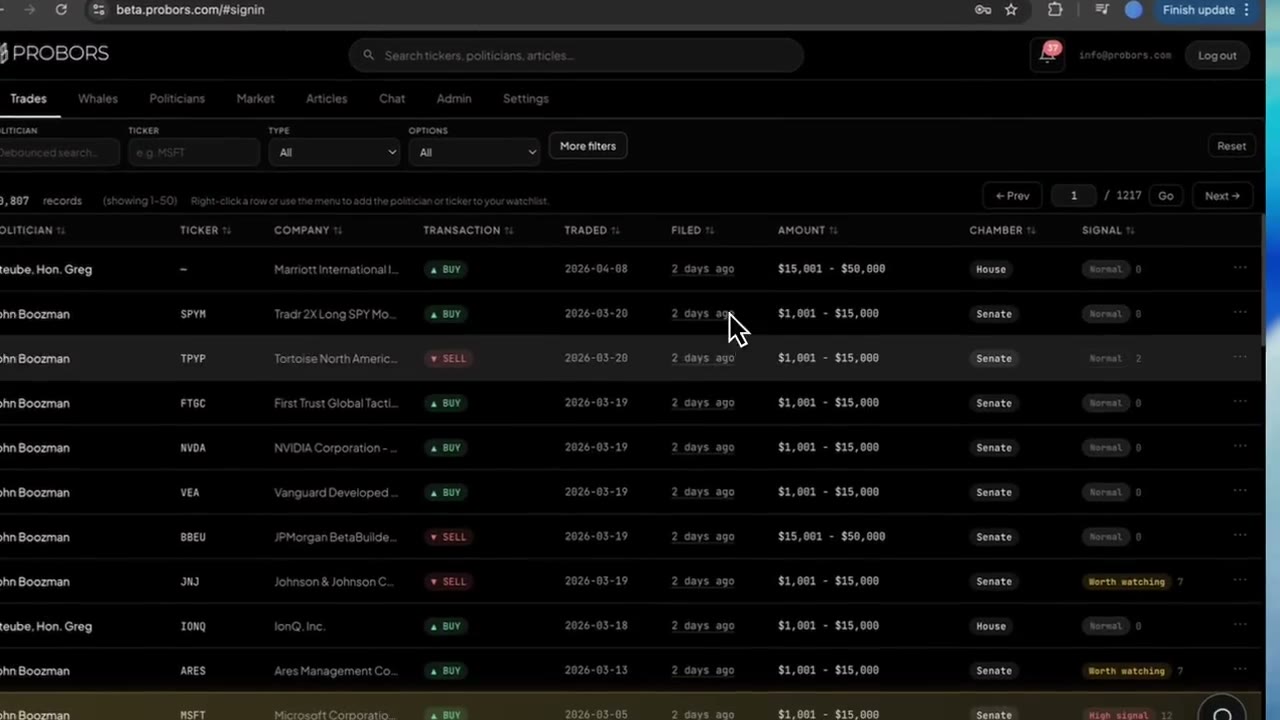

Track these trades and more on ProBors.

Sources & methodology

Last updated:

ProBors uses public disclosure records, SEC filings, House and Senate financial disclosure portals, market data, and in-product workflow checks. Articles are written as research education, not investment advice.